The largest AI Chip Manufacturer in the World

5 Things Every Investor Should Know about Taiwan Semiconductor Manufacturing Company (TSM) now

Dear Investor.

Zee here. Bonus stock analysis article for this weekend since we missed posting 17th January’s, due to a tech glitch. Here goes..

If you’ve ever wondered which company makes the chips inside your iPhone, powers AI systems like ChatGPT, or helps run your laptop, chances are it’s Taiwan Semiconductor Manufacturing Company (TSMC).

Think of TSMC as the world’s most advanced chip factory-for-hire. Unlike companies like Intel or Samsung that design AND make their own chips, TSMC only manufactures chips designed by other companies.

This makes them the go-to manufacturer for tech giants like Apple, Nvidia, and AMD. It’s like being the bakery that makes cakes for every major restaurant in town, you don’t design the recipes, but everyone depends on your ovens.

Announcement:

Join us on Monday 9th Feb 2026, for our live Free webinar “One CEO, Two Universes: Tesla Today, SpaceX Tomorrow?”.

👉🏼 Click here to reserve a spot through our Whatsapp Community. (LINK)

(Zoom link and reminders will be sent via the community)

A Quick History: From Bold Bet to Global Powerhouse

The Visionary Founder

In 1987, a 56-year-old engineer named Morris Chang made a bold decision that would change the tech world forever. After working at Texas Instruments for decades, Chang moved to Taiwan and founded TSMC with backing from the Taiwanese government and Dutch company Philips.

His revolutionary idea? Create a company that ONLY manufactures chips for others, never competing with its own customers. At the time, most people thought he was crazy. “What the hell is Taiwan doing?” was the common industry reaction. But Chang had spotted a gap: as chip-making became more expensive and complex, smaller companies needed someone to manufacture their designs without fear of competition.

The Growth Story

TSMC lost money in its first year (1987) and struggled until 1991

From 1991 onward, the company never looked back, growing steadily year after year

By 2005, TSMC captured half of the entire semiconductor foundry market

Today, TSMC accounts for nearly 45% of Taiwan’s entire stock market

The company’s stock has more than tripled in the past three years

Credit: Reuters

1. The Stock Is Hitting Record Highs

TSMC shares are on fire. The stock surged to record highs in early January 2026, jumping nearly 7% in a single day. In 2025 alone, the stock rose more than 50%, and it’s already up 8% so far in 2026. Wall Street analysts are rushing to raise their price targets, at least six major investment banks have increased their projections since the start of the year.

Goldman Sachs raised its target by a whopping 35%, while JPMorgan increased theirs by 24%. The stock is trading at around 24 times next year’s expected earnings, which analysts consider a bargain compared to other big tech companies.

2. AI Boom Is Driving Massive Growth

The artificial intelligence revolution is TSMC’s biggest growth driver right now. The company manufactures the advanced chips that power AI systems for companies like Nvidia, which is currently the hottest name in AI computing.

Wall Street expects TSMC’s revenue to grow by about 21% in 2026, impressive for a company worth nearly $1.6 trillion.

For context, the overall stock market typically grows at 10% annually, so TSMC is growing at double the market rate. In the most recent quarter, revenue jumped 40% compared to the same period last year.

3. Record Profits and Aggressive Investment Plans

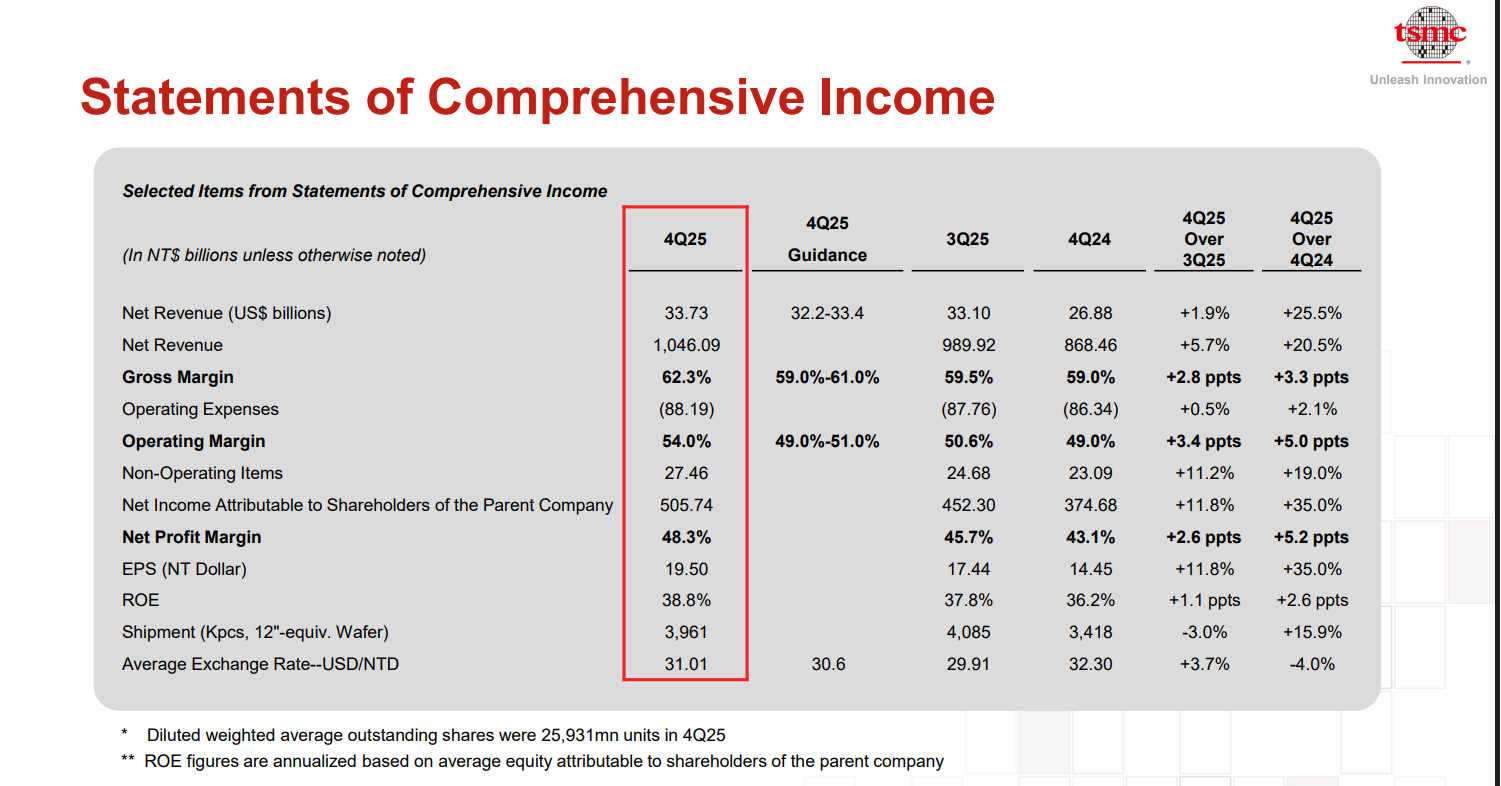

In the fourth quarter of 2025, TSMC reported its highest-ever quarterly earnings. The company’s profit margins are also extraordinary gross margins above 60%, which is exceptional in manufacturing.

For 2026, TSMC plans to spend between $52 billion and $56 billion on new equipment and facilities. That’s a huge increase from the $40.9 billion spent in 2025 and $29.8 billion in 2024.

About 70-80% of this investment will go toward the most advanced chip-making technology. This aggressive spending shows TSMC is betting big on continued demand for cutting-edge chips.

4. They’re “The Toll Booth of AI”

Analysts have started calling TSMC “the toll booth of the AI supply chain”, meaning every company building AI systems needs to go through TSMC to get their chips made. This gives TSMC a unique position: whether Nvidia, AMD, or Apple wins in their respective markets, TSMC benefits from all of them.

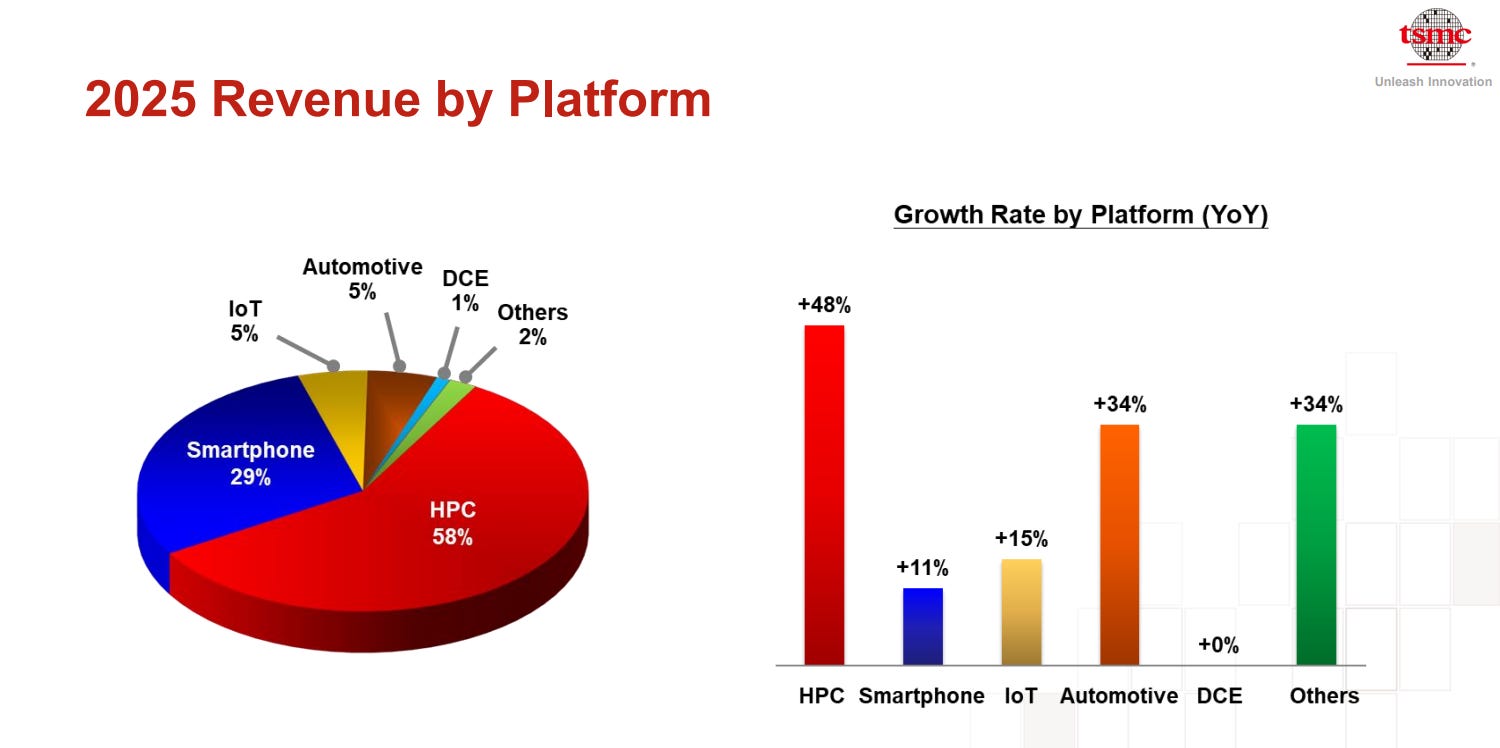

In Q3 2025, high-performance computing (which includes AI chips) accounted for 57% of TSMC’s sales, compared to 30% from smartphone chips. This shift shows how AI is becoming their core business, and it’s a trend expected to continue for years.

5. Tight Capacity Means Pricing Power

Here’s a key point for investors: TSMC’s most advanced 3-nanometer and 5-nanometer chip-making capacity is completely booked through 2027. When demand exceeds supply, companies can raise prices and that’s exactly what TSMC is doing. The company implemented price hikes in 2026, which analysts expect will push profit margins even higher.

Think of it like concert tickets for a sold-out show: when everyone wants in and there aren’t enough seats, prices go up. TSMC’s “seats” (manufacturing capacity) are fully booked by the world’s biggest tech companies.

The Bottom Line: Is TSMC a Good Investment?

For beginner investors, TSMC offers several appealing qualities:

The Pros:

Dominant market position (controls about half the foundry market)

Growing at twice the market average rate

Relatively reasonable valuation compared to other tech giants

Benefits from the AI boom without betting on any single AI company

Strong profit margins and consistent profitability

Things to Consider:

The stock has already run up significantly (up 50% in 2025)

Heavy concentration in the AI sector could be risky if AI spending slows

Geopolitical concerns around Taiwan

Cyclical industry that can experience ups and downs

Disclaimer: All information here is for educational purposes only. This is not financial advice. Please do your own research and speak with a licensed advisor before making any investment decisions. Past performance is not indicative of future returns. How we invest may not suit your investment goals and risk management profile.

Fascinating. This really make you reflect on the invisible, foundational tech that powers AI, my passion.

Really insightful piece on how TSMC's foundry model plays out when capacity gets constrained. The 'toll booth' framing is spot on, but I think the more intresting angle is how their pricing power actually compounds as process nodes shrink. Once had a friend at a fabless shop explain how switching costs go beyond just tooling, theyre tied to yield optimization that takes years to dial in. Makes me wonder if their 60% margins might actualy expand rather than compress in a cyclical downturn.