Fabrinet Is the Picks-and-Shovels Play Nobody Talks About

From a Bangkok Startup to the Heart of the AI Revolution

Dear Investors.

Zee here. While the world debates which AI company will win, a quieter story is playing out in the industrial parks of Chonburi, Thailand.

Fabrinet, a name most retail investors have never come across, manufactures the precision optical components that sit inside every major AI data centre on earth.

No flashy consumer products. No viral demos. Just extraordinarily precise manufacturing, at massive scale, for the companies building the backbone of the AI era.

Its stock has risen 250% in a year, it just posted a record quarter, and it's building one of the largest factories in Southeast Asia.

Here's what you need to know.

Announcement:

If you missed our previous webinar for “The Hidden Giant in Grab’s Business That Most Investors Overlook (Not Ride-Hailing)”

We’ll be covering it again on our Free live Webinar on Monday 20th April 2026.

Join us, especially if you’ve aways wanted to build a resilient portfolio with ETFs and stocks, and become an independent investor yourself…

👉🏼 Click here to reserve a spot. (LINK)

What does Fabrinet actually do?

Imagine you’ve invented a revolutionary new component that sits inside the world’s fastest fibre-optic cables and data centres, a tiny device that can send data at the speed of light.

You have the design and the customers, but building a factory to make thousands of these things a day, to incredibly precise tolerances, would cost you hundreds of millions of dollars and take years.

So instead, you call Fabrinet.

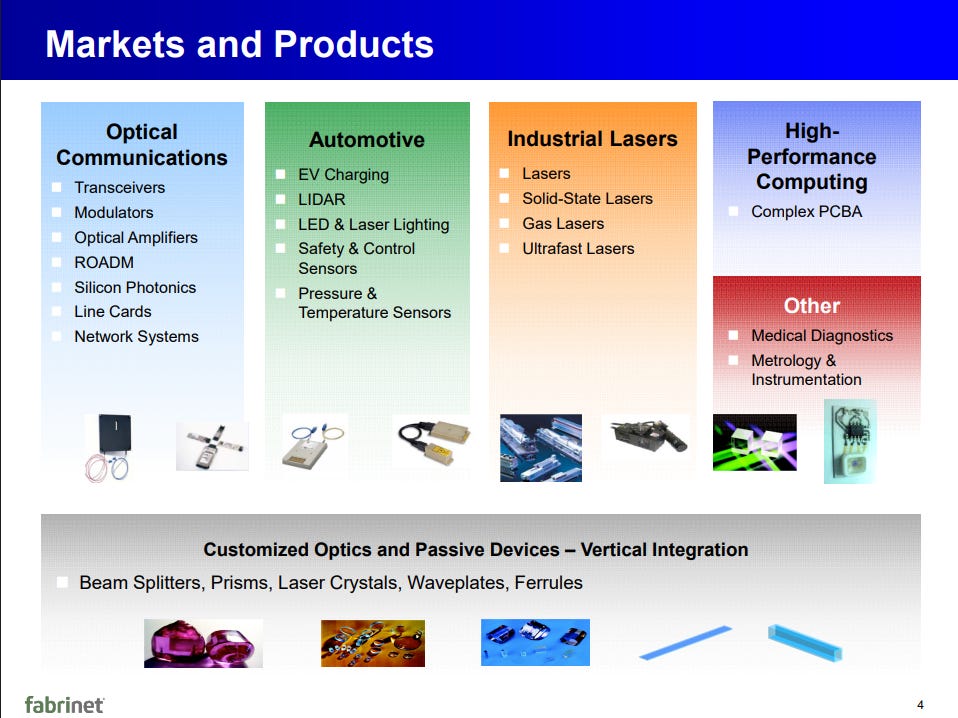

Fabrinet (NYSE: FN) is a specialist contract manufacturer based in Thailand. It builds complex optical, electro-mechanical and electronic components on behalf of the world’s leading technology companies, names like Cisco, Coherent, II-VI and others. These aren’t ordinary parts. They’re precision-engineered products used in fibre-optic communications, AI data centres, medical devices, industrial lasers, and automotive sensors. The kind of products where even a microscopic imperfection can cause failure.

Founded in 1999 and listed on the New York Stock Exchange since 2010, Fabrinet has quietly grown from a small Thai manufacturer into one of the most strategically important companies in the global tech supply chain. It employs over 16,000 people, generates more than $4 billion in annual revenue, and has become an indispensable link between the companies that design next-generation tech and the data centres and networks that power the modern world.

As AI infrastructure spending has exploded, Fabrinet has found itself in an almost uniquely privileged position, right in the middle of the supply chain for the components the AI boom simply cannot function without.

Revenue just hit a record and crushed expectations

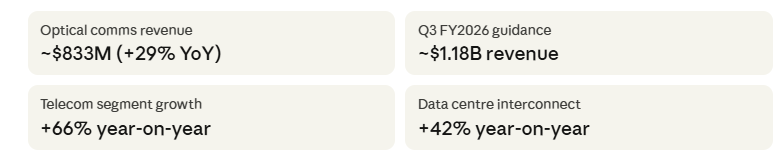

Fabrinet’s most recent quarterly results, covering the three months to December 2025, were nothing short of extraordinary. Revenue hit $1.13 billion, a record high, up 36% from the same quarter a year earlier, and up 16% compared with just the previous quarter. To put that in context, a year ago Fabrinet was doing around $830 million a quarter. The pace of growth has been dramatic.

Earnings were equally impressive. Non-GAAP (adjusted) earnings per share came in at $3.36, beating the company’s own guidance of $3.25 by about 3%.

CEO Seamus Grady called it an “exceptional quarter,” crediting multiple large strategic programmes across the business all contributing simultaneously, a sign that the growth isn’t coming from just one lucky contract but is broad-based.

AI data centres are supercharging demand and it’s only getting started

If you want to understand why Fabrinet is growing so fast, you need to understand what’s happening inside today’s AI data centres. When companies like Amazon, Microsoft, Google and Meta build the giant server farms that power AI models, they don’t just need more computers — they need an enormous amount of incredibly fast optical networking equipment to connect all those computers together. Data needs to move between thousands of servers at near-light speed, with minimal delay. The components that make that possible: transceivers, optical modules, photonic switches, are exactly what Fabrinet manufactures.

The numbers tell the story. Fabrinet’s high-performance computing (HPC) segment essentially its AI-focused business, exploded from $15 million in revenue in Q1 FY2026 to $86 million in Q2. Management expects this to reach over $150 million per quarter when fully ramped.

That’s a tenfold increase in just a few quarters, driven largely by a new relationship with Amazon Web Services. Meanwhile, data centre interconnect modules, another AI-critical product, grew 42% year-on-year, and even the traditional telecom segment surged 66%.

Fabrinet also showcased its role in the AI ecosystem at the Optical Fiber Communication Conference (OFC) 2026 in Los Angeles in March, where it hosted two investor Q&A sessions. Demonstrations and customer engagements at the event reinforced the company’s central position in co-packaged optics, optical circuit switching and next-generation interconnects, technologies that will define AI networking for the next decade.

The broad takeaway from the conference: AI data centre spending is accelerating, not slowing, and Fabrinet is positioned squarely in the path of that spend.

A new silicon photonics deal puts Fabrinet at the cutting edge of AI networking

In mid-March 2026, Fabrinet announced an expanded manufacturing partnership with iPronics, a specialist in silicon photonics technology. This is worth understanding in some detail, because it points to where AI networking is heading next.

Traditional data centre networks use electronic switches to route data, essentially, data gets converted from light to electricity, directed to the right place, then converted back to light again. This process creates latency (tiny delays) and consumes significant power. Silicon photonics-based optical circuit switching bypasses the electrical conversion entirely, keeping data as light throughout the journey. The result is faster, lower-latency, more energy-efficient networks, exactly what AI workloads demand, since large AI models require thousands of servers communicating with each other constantly at extreme speeds.

Under the expanded deal, Fabrinet is adding a dedicated production line for iPronics’ silicon photonics optical circuit switching systems, specifically targeting AI-focused data centre customers. Full operations are targeted for June 2026. This isn’t just a small add-on contract, it positions Fabrinet as a manufacturer of choice in a technology segment that many analysts believe will become a standard feature of AI data centres within the next few years. First-mover advantage in high-margin, technically complex manufacturing is exactly the kind of moat Fabrinet has historically built its business on.

A giant new factory is being built, capacity could nearly double

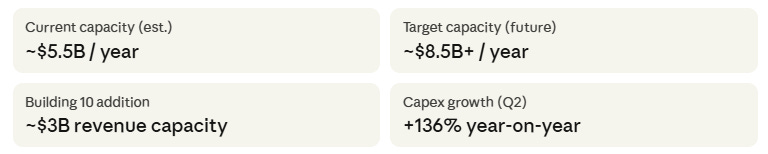

Record demand requires record capacity, and Fabrinet is making a major bet on the future. The company is currently constructing Building 10 at its Chonburi campus in Thailand, a massive 2-million-square-foot facility that will be one of the largest precision manufacturing plants in Southeast Asia. When fully ramped, management estimates it could add approximately $3 billion in annual revenue capacity on top of existing operations.

To put the scale in perspective: Fabrinet’s current manufacturing capacity is estimated at around $5.5 billion annually. Adding Building 10 and completing further conversions at its Pinehurst campus could push total capacity to $8.5 billion or more, nearly double current levels. Initial phases of Building 10 are expected to come online through the course of 2026, giving investors something concrete to watch for in upcoming quarterly updates.

The expansion is not without cost. Capital expenditures surged 136% year-on-year in Q2, briefly pushing free cash flow negative (to -$5.35 million). Total liabilities rose 55% year-on-year as the company funds the build-out. This is a deliberate, strategic investment and most analysts view it positively as a signal of genuine confidence in sustained demand but it does mean the company is in a spending cycle right now. Investors should expect capital expenditure to remain elevated through 2026 as construction continues.

In February 2026, Fabrinet also published its 2025 Corporate Responsibility Report, detailing 233 green projects that reduced electricity consumption and emissions intensity at its Thai factories. As ESG factors increasingly influence where major tech companies place their manufacturing contracts, this kind of track record matters — it's not just good optics, it's a competitive differentiator when customers are choosing between suppliers.

The stock has had a massive run, here’s what could go wrong

Fabrinet’s stock has risen almost 250% in the past year alone, climbing from around $174 to a record high of $679 in April 2026. That kind of run reflects genuine business momentum, but it also means the bar for disappointment is now very high.

(I) Valuation

Fabrinet trades at a trailing price-to-earnings ratio of roughly 53x, meaning investors are paying $53 for every $1 of current earnings. The forward P/E (based on expected future earnings) is a more reasonable 13x, reflecting how fast earnings are growing. The PEG ratio (which adjusts for growth) sits at around 1.19, not cheap, but not bubble territory either.

Analyst consensus price targets cluster between $530 and $582, with some optimistic forecasts reaching $715. The fact that current prices are above most analyst targets is worth noting.

(II) Customer concentration

Fabrinet’s revenues are heavily dependent on a handful of large technology customers. If one or two of those customers slows orders, because their own AI buildout pauses, because they bring manufacturing in-house, or because demand softens, Fabrinet’s revenue could drop sharply. This is a structural risk in the contract manufacturing business model.

(III) Leadership transition

In October 2025, Tom Mitchell, the founder who built Fabrinet from a startup in 2000 into the company it is today, retired after 25 years. He had already handed over the CEO role to Seamus Grady in 2017, but his departure as Chairman nonetheless removes one of the company’s most knowledgeable long-term stewards at a pivotal moment of growth. Grady has performed well, but it’s a transition worth monitoring.

(IV) Insider selling

CEO Grady sold 22,451 shares in a single day in November 2025, and director Thomas Kelly sold additional shares in February 2026. Insider selling doesn’t always signal a problem, executives often sell shares for personal financial planning — but large single-day sales by senior figures are always worth being aware of as an investor.

(V) Margin pressure

Heavy capital investment in new facilities, combined with the complexity of ramping up new production lines, creates execution risk. If Building 10 takes longer than expected to ramp, or if new programmes like iPronics silicon photonics prove harder to scale than anticipated, margins could come under pressure in the near term.

What to watch next:

Fabrinet's next earnings call is scheduled for 4 May 2026.

Key things to listen for: the pace of Building 10 construction and when it begins contributing revenue, progress on the iPronics silicon photonics ramp, any commentary on co-packaged optics adoption timelines, and whether the HPC segment is tracking toward management's $150M+ quarterly target.

Guidance for Q4 FY2026 will also give investors a clearer picture of whether the current growth trajectory is sustainable through the rest of the year.

Disclaimer: All information here is for educational purposes only. This is not financial advice. Please do your own research and speak with a licensed advisor before making any investment decisions. Past performance is not indicative of future returns, and that’s exactly the point.