Is Grab Your Gateway to Southeast Asia's Tech Boom?

How Grab (NASDAQ:GRAB) became the region's digital infrastructure, and finally turned profitable

Dear Investors.

Zee here. Picture this: You’re in Jakarta, Singapore, or Manila. You need a ride to the airport. You’re hungry and want dinner delivered. You need to send a package across town. You want to book a table at a restaurant. You even need a place to park some spare cash for better returns than your savings account.

There’s one app for all of that: Grab.

If you’ve spent any time in Southeast Asia, you’ve probably used Grab without thinking twice about it. It’s become as embedded in daily life as Google or Amazon is in the West. But here’s what most people don’t realize: this familiar green app just achieved something remarkable that could reshape how investors think about Southeast Asian tech companies.

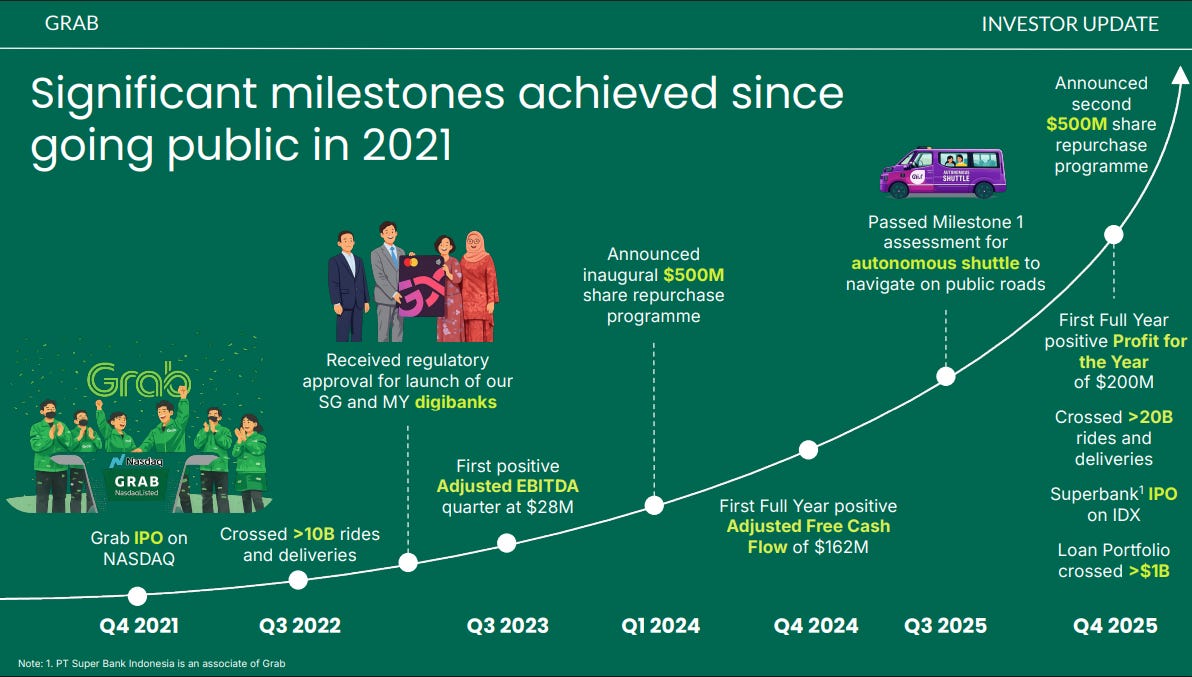

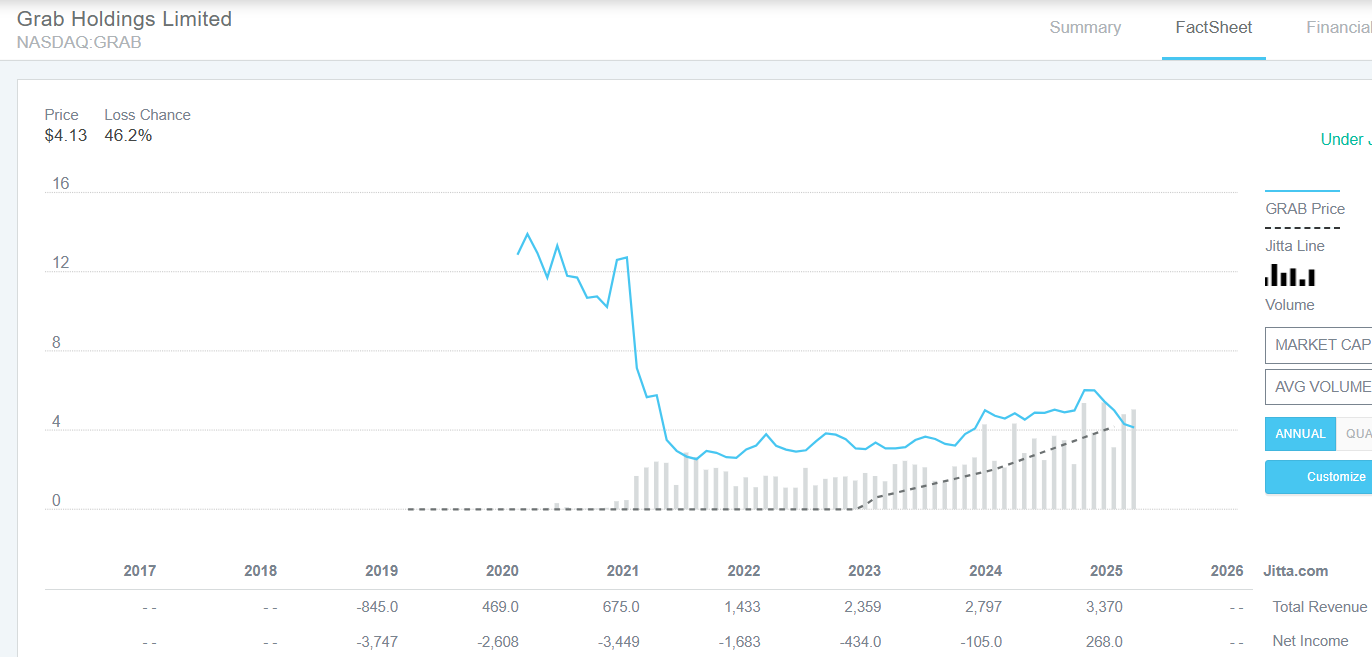

In February 2025, Grab (NASDAQ:GRAB) announced its first-ever full-year profit. After more than a decade of aggressive expansion, eye-watering cash burn, and skepticism from Wall Street, the company finally proved it could make money while serving hundreds of millions of people across eight countries.

Yet when this milestone was announced, something strange happened: the stock dropped 2%.

So what exactly is this company, and why should investors care? Understanding Grab means understanding where one of the world’s fastest-growing regions is headed.

Let’s break down Grab’s recent milestone, explore its journey from scrappy startup to regional champion, and examine what makes it special.

Announcement:

Join us on Wednesday 18th March 2026, for our live Free webinar “Stock Investing or ETF Investing: Which is better?”.

👉🏼 Click here to reserve a spot. (LINK)

A Quick History: From Taxi App to Super App

Grab started in 2012 as MyTeksi, a simple taxi-hailing app in Malaysia founded by Anthony Tan and Tan Hooi Ling. Think of it as Southeast Asia’s answer to Uber. In fact, Grab grew so strong that Uber actually gave up and sold its Southeast Asian operations to Grab in 2018.

But Grab didn’t stop at rides. Over the years, it expanded into food delivery (GrabFood), grocery delivery (GrabMart), package delivery (GrabExpress), and even financial services (digital payments and lending). Today, it operates across eight countries in Southeast Asia, including Singapore, Malaysia, Indonesia, Thailand, Vietnam, and the Philippines.

In 2021, Grab went public on the NASDAQ stock exchange through a SPAC merger, raising billions of dollars.

It was a big moment for Southeast Asian tech.

Here are five key things from Grab’s latest earnings report that investors should understand:

1. Grab Just Made Its First Full-Year Profit Ever

After years of losing money while building its business, Grab finally turned profitable for an entire year in 2025. This is a huge deal because it shows the company isn’t just growing, it’s growing sustainably.

The company achieved 20% revenue growth in Q4 2025, which means it’s bringing in a lot more money than before. Yet surprisingly, the stock price dropped 2% after this announcement.

Why? More on that later.

2. Three Business Segments Working Together

Think of Grab as having three main money-makers:

Mobility (Ride-hailing): This is the bread and butter. When you book a ride, Grab makes money. This segment has excellent profit margins of about 44% and contributes roughly 74% of the company’s overall profits. People started using Grab for rides, and they stay for everything else.

Delivery (Food and Groceries): This segment has the highest customer conversion rate at 24%, meaning when people use the app, they’re very likely to order something. However, profit margins are lower at around 10%. To boost profits, Grab is adding advertising (GrabAds) where restaurants and stores pay to be featured prominently in the app.

Fintech (Digital Payments and Lending): This is the sleeping giant. Grab used to just connect people with loans from banks and take a small fee. Now, it’s lending its own money, which means it can keep more of the interest earned. While this segment isn’t profitable yet, Grab expects it to turn profitable by the second half of 2026. The loan portfolio is expected to nearly double in 2026.

3. The Secret Weapon: GrabMaps

Here’s something most people don’t know: Grab has its own mapping technology called GrabMaps. While competitors like Uber and Foodpanda use Google Maps, Grab built its own system that knows every small street and alleyway in Southeast Asia.

Why does this matter? Because better maps mean drivers take faster, cheaper routes. This gives Grab higher profit margins than competitors on every delivery. It’s updated in real-time by thousands of drivers, making it incredibly accurate. This is why Uber left Southeast Asia and why competitors struggle to compete, they simply can’t match Grab’s efficiency.

4. Growth Through Smart Acquisitions

Grab doesn’t just grow by attracting new users—it also buys other companies to expand its services. Recent examples include:

Jaya Grocer in Malaysia (a premium grocery chain)

Chope (a restaurant reservation platform)

Trans-cab (a taxi company)

Stash (a US-based investment platform)

These acquisitions help Grab offer more services, which keeps users inside the Grab app for more of their daily needs.

The more services you use, the less likely you are to switch to a competitor.

5. Room to Grow: Only Scratching the Surface

Here’s the exciting part for long-term investors: Grab currently operates mainly in Tier 1 cities (big urban areas). The vast majority of Southeast Asia’s population is still untapped. The company believes it can achieve 20% annual growth through 2028 just by expanding to more people in urban areas.

Grab also projects a compound annual growth rate (CAGR) of 20% from 2025 to 2028, which means revenues could nearly double in just three years.

The Bottom Line for Investors

Grab has several advantages its competitors don’t:

A strong balance sheet with lots of cash and minimal debt

GrabMaps giving it a cost advantage

No real competitor in Southeast Asia with the same resources

Growing profitability across all segments

Grab is transitioning from a money-losing growth company to a profitable infrastructure player in Southeast Asia. It’s embedded in daily life for millions of people for transportation, food, shopping, and increasingly for financial services.

The company achieved its first full-year profit in 2025, is growing at 20% annually, and has significant room to expand beyond major cities. While the market seems skeptical about cash burning, Grab’s unique advantages (especially GrabMaps) and strong financial position suggest it can defend its dominance.

For investors, Grab represents a bet on Southeast Asia’s digital economy. If you believe that region will continue growing and that more people will use apps for daily services, Grab is positioned to benefit.

The key question is whether the market is underestimating Grab’s transformation from an unprofitable startup to a profitable regional infrastructure company. Only time will tell.

Disclaimer: All information here is for educational purposes only. This is not financial advice. Please do your own research and speak with a licensed advisor before making any investment decisions. Past performance is not indicative of future returns. How we invest may not suit your investment goals and risk management profile.