The Hotel Giant That Doesn't Own Hotels

Marriott just beat earnings again. How a company with almost no real estate keeps compounding like clockwork.

Dear Investor.

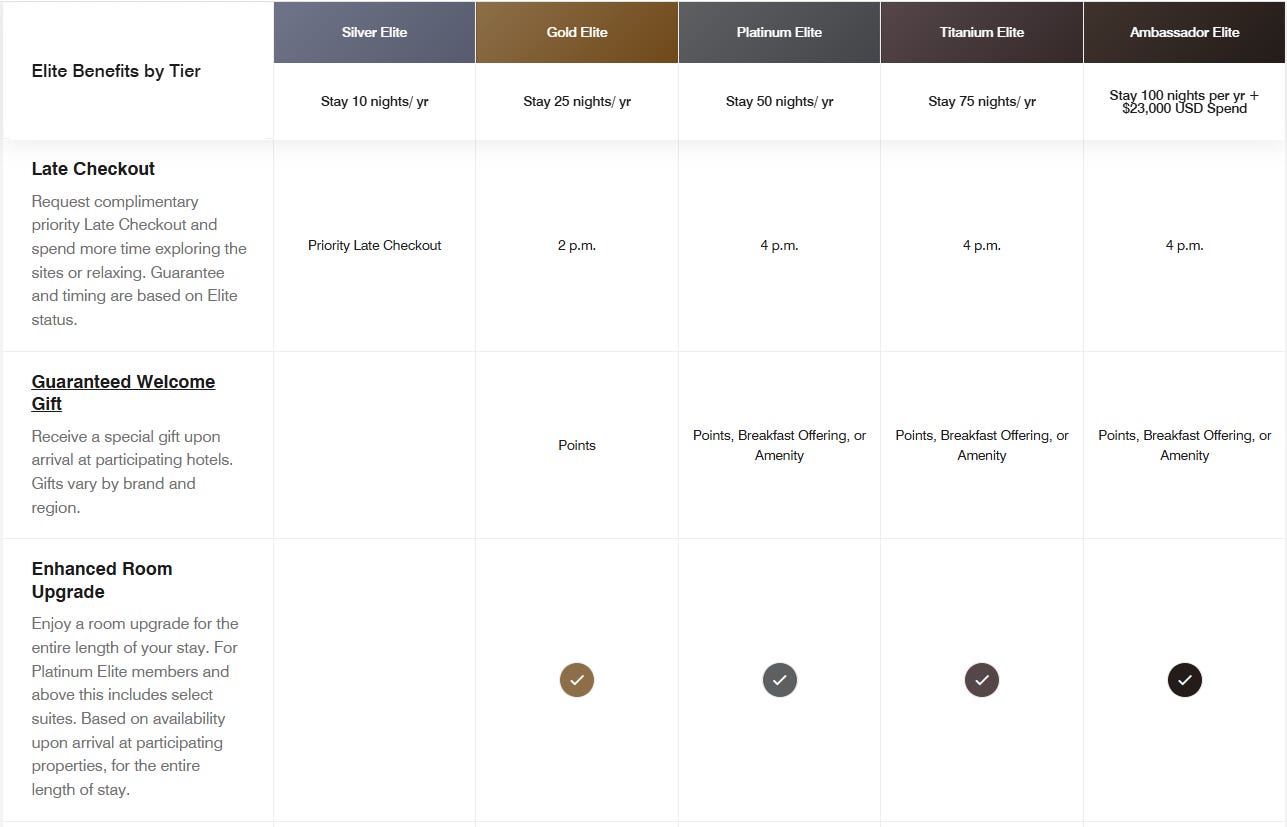

Zee here. Recently, my friend and also our student Jonathan shared a clever travel hack for the Marriott Bonvoy program: instead of the usual 50-nights requirement, he qualified for Marriott Bonvoy Platinum through a 16-nights challenge.

He then used a strategy of selling options (we teach this in our classes too) to offset the cost of those 16 nights, effectively letting the stock market help fund his hotel stays.

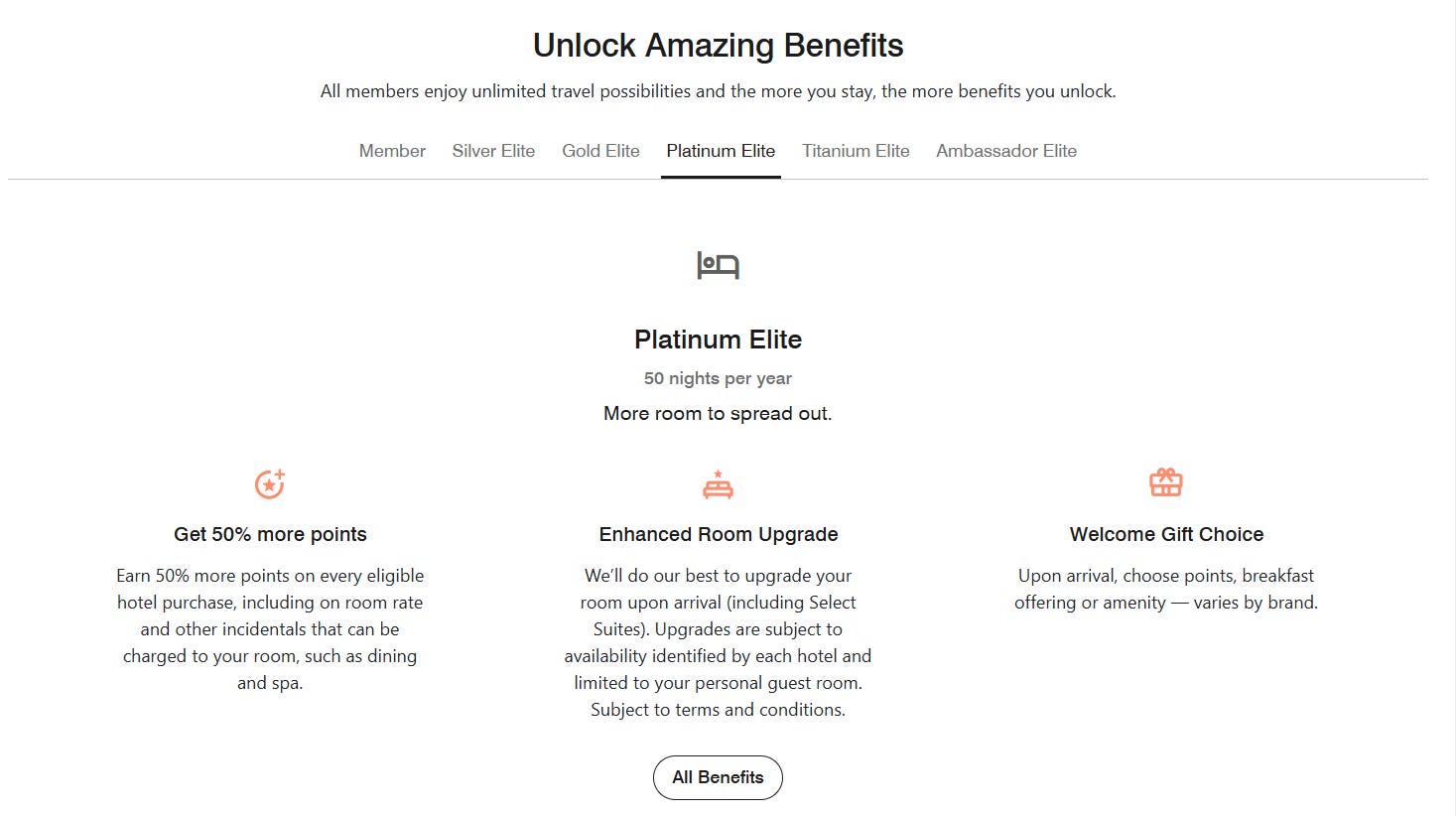

The payoff: Marriott Bonvoy Platinum status, unlocking suite upgrades (when available), lounge access, and a relaxed 4pm late checkout.

That got me digging into how Marriott structures its loyalty ecosystem and business model, and how programs like this are designed not just to reward travel, but to drive repeat stays and long-term brand loyalty.

Marriott International (NASDAQ: MAR) has delivered strong share price performance in recent years, with the stock rising more than 50% over the past year and over 140% over the last five years.

The gains have been supported by resilient global travel demand, particularly in higher-end and luxury hospitality segments, which have contributed to broader strength across the hotel industry.

During the same period, the broader hotel and motel industry gained roughly 23%, meaning Marriott has materially outperformed many of its industry peers.

In case you missed the last one...

Join us on Monday 25 May 2026 (7:30-915pm SGT), for our live Free webinar, where we cover:

* Our resilient investing strategy that we use in our public portfolio

* Stock Analysis: Will Visa be disrupted by AI?

Attendees will also get preview our new AI Powered Stock Market Simulator game where you’ll learn about your investing strengths and weakness.

👉🏼 Click here to reserve a spot. (LINK)

How Does Marriott Make Money?

Here’s the thing most people get wrong about Marriott. They think it’s a hotel company as in, it owns hotels.

It doesn’t. Not really.

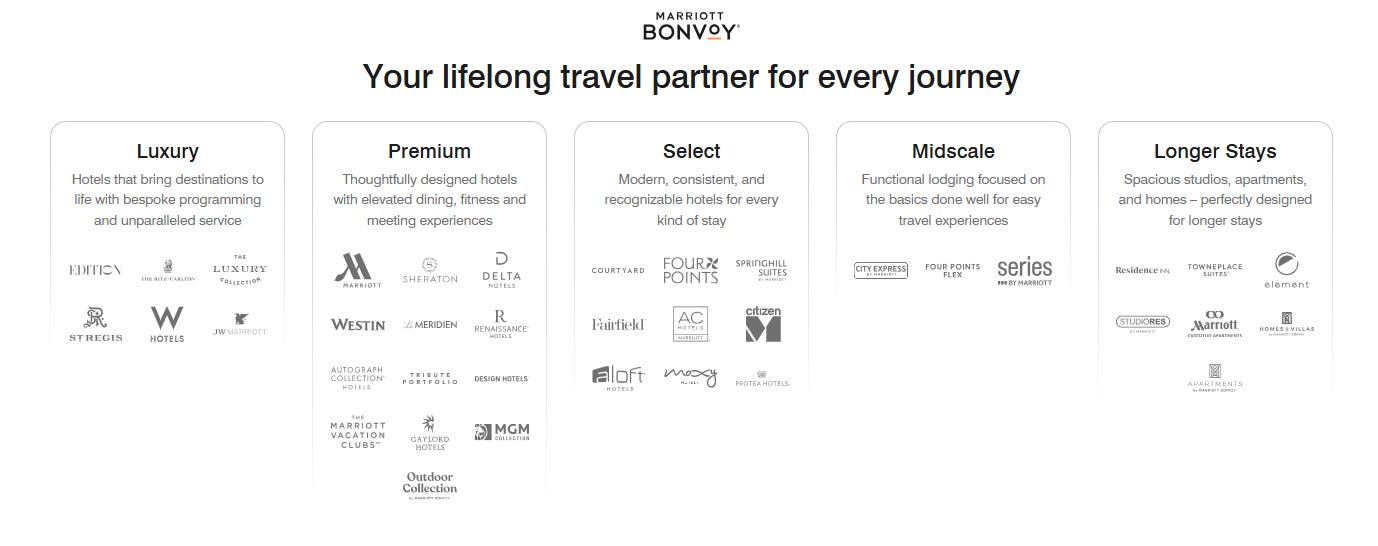

Marriott’s actual business is collecting fees. It manages and franchises hotels that are owned by other investors and real estate developers. Someone else builds the property, takes on the debt, and bears the construction risk. Marriott lends its brand: Sheraton, Westin, W Hotels, Ritz-Carlton, Courtyard, and more than 30 others and collects a percentage of revenue for doing so.

Think of it like a franchise system. A franchisee opens a McDonald’s, invests their own capital, and pays McDonald’s a royalty. Marriott works the same way, just with beds instead of burgers.

This “asset-light” model is what makes Marriott so interesting as an investment. When hotels do well, Marriott earns more in fees. When hotels struggle, the pain falls mostly on the property owners, not Marriott. The company gets upside exposure to travel, without carrying the full downside of owning physical real estate.

1. They Just Beat Earnings And Raised Their Outlook

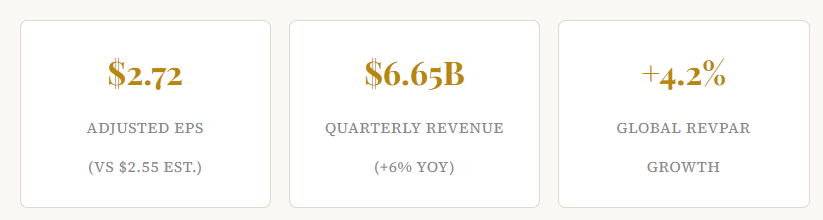

Marriott’s Q1 2026 results came in stronger than Wall Street expected. Adjusted earnings per share reached $2.72, beating the analyst forecast of $2.55 by a meaningful margin. Revenue for the quarter came to $6.65 billion, up 6% compared to the same period last year.

The key metric for any hotel company is RevPAR, revenue per available room. It’s essentially a measure of how much money each hotel room is generating on average. Global RevPAR increased 4.2% during the quarter, helped by improvements in both occupancy rates and average daily room prices.

Following the beat, management slightly raised its full-year adjusted EPS guidance to $11.51 at the midpoint. When a company beats and raises, it usually tells you that demand is holding up better than feared.

2. Marriott Portfolio Is Growing Fast

One of the most underappreciated parts of Marriott’s story is how relentlessly it keeps adding new rooms to its system. More rooms means more fees. More fees means more earnings, without Marriott needing to spend its own money building anything.

Marriott added roughly 15,900 net rooms during the quarter, expanding its worldwide portfolio to more than 9,900 properties with nearly 1.8 million rooms.

Marriott’s development pipeline reached a record 4,107 properties representing nearly 618,000 rooms, with 43% of those rooms currently under construction. That’s future fee income already in the works and the company didn’t have to build any of it.

For long-term investors, this pipeline is the engine. Even in a year where travel demand softens, room growth compounds the fee base. Marriott has guided for net rooms growth of 4.5% to 5% for the full year 2026, a pace that quietly but steadily expands the business.

3. Bonvoy Is Becoming a Business in Its Own Right

Marriott Bonvoy is the company’s loyalty programme, it has over 271 million members. Most people think of loyalty points as just a marketing gimmick. But for Marriott, Bonvoy has become a genuine revenue engine.

The programme is linked to co-branded credit cards issued by banks like Chase and American Express. Every time a Bonvoy cardholder swipes their card, Marriott earns a royalty fee.

The headline catalyst for 2026 is a projected 35% jump in co-branded credit card fees, loyalty-linked products that collect royalties from card partners, driven by both a renegotiated royalty rate and continued high-spend growth across Marriott’s 34-card, 11-country Bonvoy program.

This is a meaningful diversification of income. Hotel fees move with travel demand. Card royalties move with consumer spending more broadly. It makes the business stickier and more resilient over time.

The Bonvoy app and platform also give Marriott direct access to its guests, reducing reliance on booking platforms like Expedia or Booking.com, which typically take a cut of every reservation.

The more guests book directly through Bonvoy, the more margin Marriott keeps.

4. The Middle East Is a Real Headwind Right Now

Not everything is going Marriott’s way.

The ongoing conflict in the Middle East has been materially disrupting travel across the region. The outlook assumes continued Middle East travel disruption, including an expected roughly 50% RevPAR decline in the region during the second quarter, which would reduce full-year global RevPAR growth by 100 to 125 basis points.

Management has assumed Middle East disruptions continue through the end of 2026. The Middle East accounts for about 3% of Marriott’s open rooms but around 7% of its development pipeline, meaning future growth in the region is also at risk of delay.

To put it simply: a 100 to 125 basis point drag on RevPAR growth is meaningful when you’re guiding for 2% to 3% total. It shaves a significant chunk off an already modest target.

The silver lining? Marriott’s international diversification means no single region can derail the business. The company added more than 7,300 net rooms in international markets just in Q1 alone, and Asia-Pacific in particular continues to post strong growth.

The Middle East pain is real, but it’s also contained.

5. They Are Returning a Lot of Cash to Shareholders

One of the privileges of an asset-light business is that it generates cash without needing to constantly reinvest in physical assets. Marriott has been putting that cash to work, returning it to shareholders through buybacks and dividends.

During the quarter, Marriott repurchased 2.1 million shares for approximately $700 million. Including dividends and buybacks, the company has returned more than $1.2 billion to shareholders so far this year through April 29.

For the full year 2026, gross fee revenue is guided to rise 8% to 10% in 2026, with adjusted EPS growth projected at 13% to 15%, materially above the revenue growth rate, reflecting operating leverage and a meaningful reduction in share count from over $4.3 billion in planned capital returns.

That last part is worth pausing on. EPS growing faster than revenue is a classic sign of buyback leverage, fewer shares outstanding means each remaining share earns a bigger slice of the pie. If management executes on that $4.3 billion return target, shareholders benefit even if revenue growth is modest.

Bottom line

Marriott is a genuinely well-constructed business. The fee model insulates it from the capital-heavy risks of owning real estate. The Bonvoy loyalty platform is becoming an asset in its own right. The development pipeline is compounding quietly in the background. And the capital return programme rewards patient shareholders.

The risks are real too, a heavy debt load of $16.5 billion, sensitivity to geopolitical disruption, and a valuation that prices in a lot of continued growth already. This is not a “screaming bargain” stock. It is, however, a high-quality business that serious investors should understand.

Disclaimer:

All information here is for educational purposes only. This is not financial advice. Please do your own research and speak with a licensed advisor before making any investment decisions. Past performance is not indicative of future returns. How we invest may not suit your investment goals and risk management profile.