War? What War? Corporate America Is Making More Money Than Ever Before.

While markets shake and headlines warn of instability, S&P 500 margins quietly hit a record 15%.

Dear Investor.

Zee here. We published slightly later this week as we changed to a more timely article—one that is particularly relevant in today’s fearful market conditions.

When the stock market dips, it’s natural to feel uneasy. The headlines get louder, the numbers turn red, and it can feel like something has gone fundamentally wrong with the economy. But sometimes, and this is one of those times, the deeper story is actually a very positive one.

Underneath all the short-term noise, the companies that make up the S&P 500 are doing something remarkable: they are earning more profit on every single dollar of sales than at any point in recorded history.

That is not a small detail.

It is one of the most important signals you can look at when trying to understand the health of your investments.

Announcement:

If you missed our previous webinar for “The Hidden Giant in Grab’s Business That Most Investors Overlook (Not Ride-Hailing)”

We’ll be covering it again on our Free live Webinar on Wednesday 20th April 2026.

Join us, especially if you’ve aways wanted to build a resilient portfolio with ETFs and stocks, and become an independent investor yourself…

👉🏼 Click here to reserve a spot. (LINK)

What is a profit margin, and why does it matter?

Let’s start with the basics. A profit margin is simply the percentage of revenue that a company gets to keep after paying all of its costs — wages, rent, raw materials, taxes, and everything else.

If a company earns $15 in profit from every $100 of sales, its profit margin is 15%.

It’s a powerful number. Two companies can have the same total sales figures, but the one with a higher profit margin is the stronger business. It means the company is running efficiently, has pricing power over its competitors, and has room to weather difficult periods without cutting staff or slashing investment.

For investors, rising profit margins across the entire S&P 500 (500 of America’s largest companies) is about as positive a signal as you can find. It means the broad economy of public companies is becoming more productive, not less.

Here are the numbers

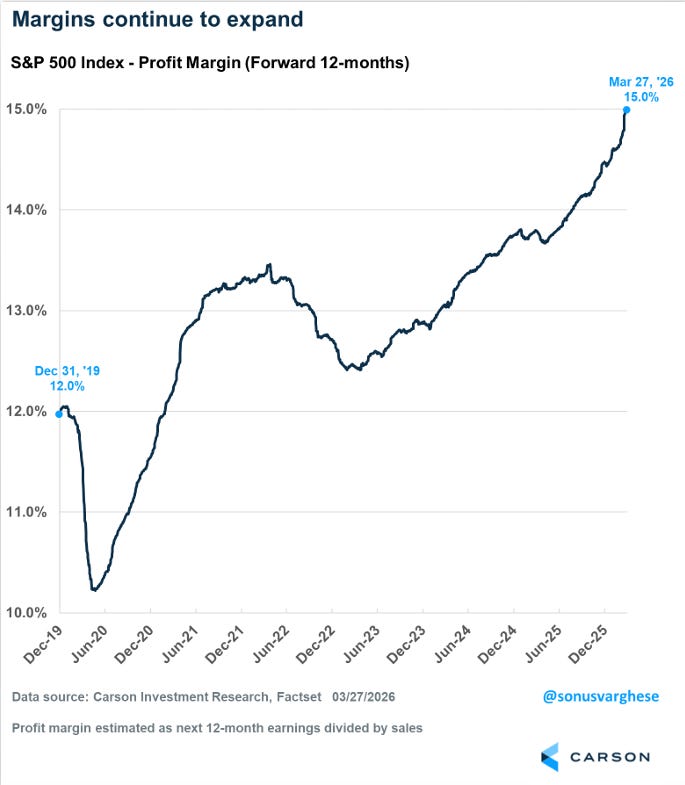

Current S&P 500 profit margin: 15% (An all-time record)

Pre-pandemic in December 2019: 12%

The pandemic test and how companies passed it

To appreciate how impressive today’s numbers are, it helps to remember what happened just a few years ago. When the pandemic hit in early 2020, corporate profit margins cratered. Supply chains seized up, costs spiraled, and demand evaporated almost overnight. Margins dropped sharply, a totally understandable response to one of the most disruptive global events in a century.

But rather than simply recovering back to their old levels, companies came back stronger. The crisis forced boardrooms across America to rethink how they operate: automating repetitive tasks, renegotiating supplier contracts, restructuring workforces, and investing heavily in technology. The result was not just a recovery, it was a transformation.

By late 2021, margins had already clawed back to pre-pandemic levels. And since then, they have kept climbing, steadily, year after year, until arriving at today’s record of 15%.

What’s driving the margin expansion?

Three forces are working together to push margins higher.

First, technology investment is paying off. The wave of spending on cloud computing, automation, and artificial intelligence that dominated corporate budgets for the past five years is now showing up as real efficiency gains. Companies are doing more with fewer people and doing it faster.

Second, pricing power has proved remarkably durable. During the inflation spike of 2022 and 2023, many analysts predicted that consumers would push back hard on higher prices and force companies to absorb their rising input costs. Instead, the opposite largely happened, companies passed costs on to customers and held their ground. That pricing confidence has not fully unwound.

Third, the composition of the S&P 500 itself has shifted. The index is now dominated by large technology and services businesses, which naturally carry higher margins than traditional manufacturers or retailers. As these companies have grown, they have pulled the overall index average upward with them.

Doesn’t a market pullback mean something is wrong?

Not necessarily and this is perhaps the most important point for everyday investors to understand. Stock prices fluctuate based on a cocktail of factors: interest rate expectations, geopolitical headlines, investor sentiment, and short-term economic data. None of these things have to move in lockstep with underlying corporate profitability.

What the margin data tells us is that the current period of weakness is about how much investors are willing to pay for earnings, not about the earnings themselves disappearing. The market has gone from pricing stocks at a premium to pricing them at something closer to fair value. That is healthy. It creates a better entry point for long-term investors and reduces the risk of a more serious correction later.

Think of it like a high-street store that has been running a record-breaking year of sales, but whose share price has slipped because one analyst wrote a cautious note about the economy. The underlying business has not changed only the emotions of the room.

The bigger picture for your portfolio

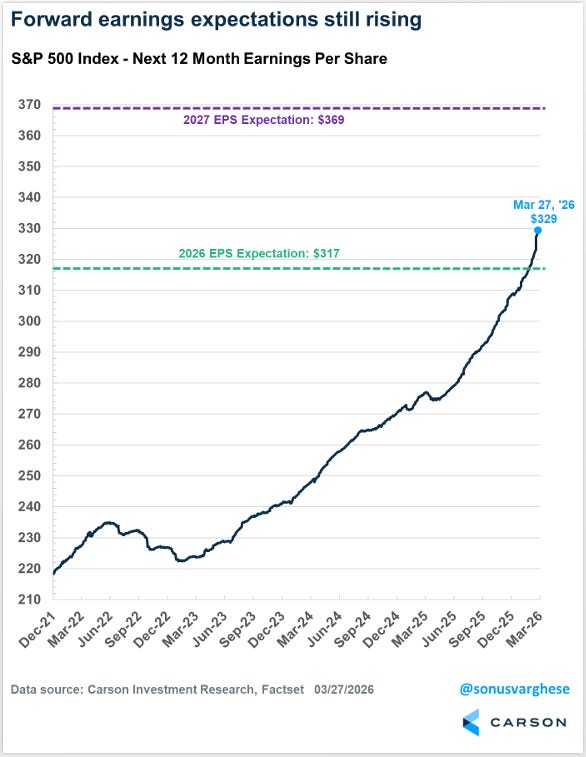

The recent market pullback has been driven almost entirely by valuation drop — investors are simply paying less per dollar of future earnings. It has not been caused by a collapse in those earnings themselves. Forward earnings estimates for the S&P 500 keep rising even as stock prices have wobbled.

A market that falls because profits are collapsing is a very different animal from one that falls because sentiment has cooled on already-healthy businesses.

But here is the takeaway that matters for long-term investors: the engine underneath the American economy’s largest companies is running better than it ever has. Businesses are leaner, more profitable per dollar of revenue, and still growing their forward earnings estimates despite external headwinds.

History has consistently rewarded investors who looked past short-term noise and stayed anchored to what businesses are actually doing.

Disclaimer: All information here is for educational purposes only. This is not financial advice. Please do your own research and speak with a licensed advisor before making any investment decisions. Past performance is not indicative of future returns, and that’s exactly the point.