Inside Mastercard's Quiet Empire

Why Mastercard's business model is one of the most resilient structures in modern finance

Dear Investor,

Zee here. After our deep-dive on Visa previously, several of you asked for the same on Mastercard, Visa’s quieter, arguably more interesting rival.

At first glance, the two companies look almost identical: both own payment networks, both earn fees on every transaction, both are absurdly profitable.

But spend a little time under the hood and the differences start to matter, especially right now, when Mastercard is making some of the boldest bets in its history on AI, stablecoins, and a future where software agents do your shopping for you.

In case you missed the last one...

Join us on Monday 25 May 2026 (7:30-915pm SGT), for our live Free webinar, where we cover:

* Our resilient investing strategy that we use in our public portfolio

* Stock Analysis: Will Visa be disrupted by AI?

Attendees will also get preview our new AI Powered Stock Market Simulator game where you’ll learn about your investing strengths and weakness.

👉🏼 Click here to reserve a spot. (LINK)

What Does Mastercard Actually Do?

Every time someone taps a Mastercard at a shop, pays online, or moves money across borders, Mastercard’s network invisibly connects the buyer’s bank to the seller’s bank in seconds. For providing that connection, Mastercard charges a small fee.

Here’s what makes this business model special:

• Mastercard does NOT lend money or hold customer deposits, that’s the bank’s job

• Mastercard earns a small ‘toll’ on every transaction that crosses its network

• It operates in over 210 countries, processing billions of transactions per day

• The more global commerce grows, the more Mastercard earns automatically

Think of it like owning the road, not the cars. Mastercard doesn’t care whether you buy shoes or a car, it just wants traffic on its highway.

This ‘asset-light’ model means very high profit margins and strong, consistent cash flows.

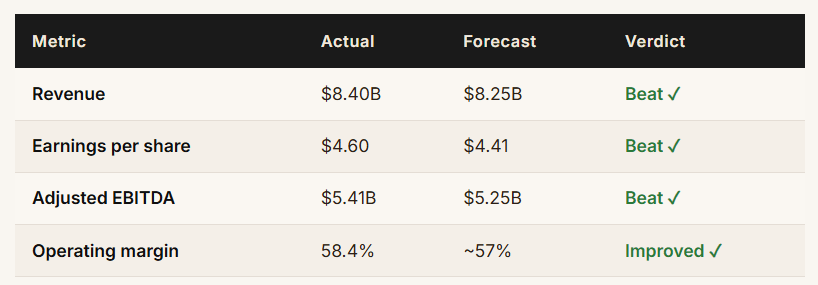

1. Strong results but geopolitics caused a stock dip

Mastercard beat every target in Q1 2026.

Despite all this, the stock fell after the report. The culprit: cross-border travel spending.

When people travel internationally and spend abroad, Mastercard earns higher fees than on domestic transactions. The ongoing conflict in the Middle East dampened international flights and tourism, creating a meaningful dent in one of Mastercard's most profitable revenue lines.

2. Services now make up 40% of revenue and they’re growing twice as fast

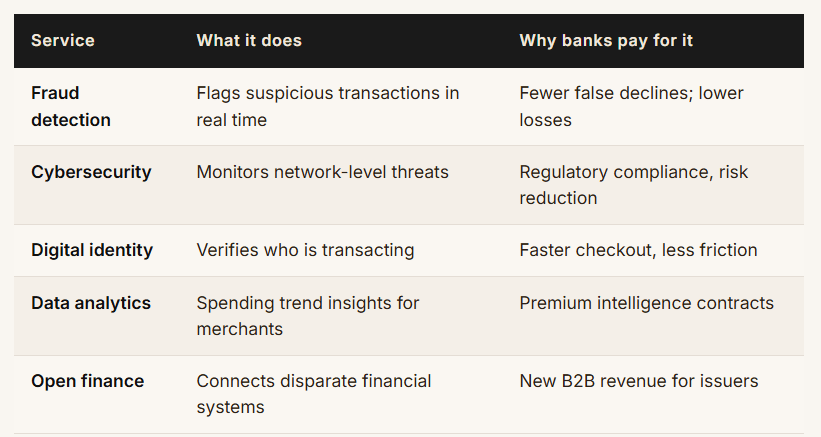

Here’s the part of the Mastercard story that doesn’t get enough attention: the company has quietly become a financial technology services business, not just a payment processor.

These “Value Added Services and Solutions” (VASS), fraud tools, cybersecurity software, data analytics, digital identity verification grew 18% year-on-year and now represent approximately 40% of total net revenue. A decade ago, this number was negligible.

Why does this matter to investors? Two reasons.

First, these services are stickier than transaction fees, banks sign multi-year contracts and rarely switch.

Second, they're less cyclical: even if spending slows in a downturn, financial institutions still need fraud detection and cybersecurity. Services provide a buffer that pure payment revenue cannot.

3. A $1.8 billion bet on the future of money

In March 2026, Mastercard announced it would acquire BVNK, a company that builds infrastructure for stablecoins for up to $1.8 billion, including $300 million in performance-based payments.

If you haven’t heard of stablecoins, they’re digital currencies pegged to a real-world asset like the US dollar. Think of them as digital cash that can travel across the internet instantly, cheaply, and without a bank in the middle.

BVNK already powers stablecoin infrastructure for financial institutions across multiple markets. Acquiring it means Mastercard can now offer a complete bridge between traditional banking rails and the crypto world, letting clients pay out in stablecoins, settle cross-border invoices instantly, and accept digital assets alongside regular currency.

As regulatory frameworks for stablecoins come into focus, in the US, EU, Singapore, and the UK, the commercial opportunity grows. Businesses that want to pay international suppliers in stablecoins, or offer customers digital dollar wallets, will need infrastructure to do so. Mastercard wants to be that infrastructure.

4. Mastercard is building an AI

Most companies talk about using AI. Mastercard is doing something more interesting: building its own.

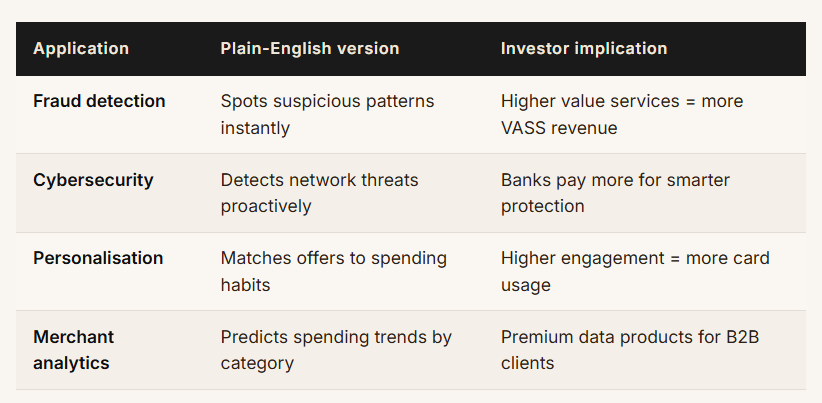

The company is developing what it calls a Large Tabular Model (LTM), its own foundation AI trained not on text or images like ChatGPT, but on billions of anonymized payment transactions. Working with Nvidia and Databricks, the model learns patterns across spending behavior, fraud signatures, merchant data, and authorization events.

Because all personal data is stripped before training, privacy is protected but the patterns remain. The model can learn to predict which transactions look fraudulent before the card is declined, which merchants are growing before the data is public, and which offers a cardholder is most likely to respond to.

Here's the key insight: unlike a general AI tool that any company can license, Mastercard's LTM is trained on data only Mastercard has. No competitor, not Visa, not any fintech, can replicate this without decades of equivalent transaction history. It is, in the truest sense, a competitive moat built from data.

5. AI is about to start spending money and Mastercard wants to be the trust layer

This is the most forward-looking story in Mastercard’s portfolio, and possibly the most significant for long-term investors.

We are at the early edge of “agentic commerce”, a world where AI assistants don’t just recommend things but actually buy them on your behalf. Imagine telling your AI: “Book me a return flight to Tokyo next month, under $1,200, aisle seat.” And it just does it — no checkout page, no card details, no confirmation to forward.

For this to work at scale, there needs to be a trusted payment layer that can verify: Is this AI agent authorized to spend? Was the purchase within pre-set limits? Is the merchant legitimate? That’s exactly what Mastercard’s Agent Pay programme provides.

Mastercard has already completed authenticated agentic transactions in Singapore with DBS and UOB, the first live, verified AI-initiated payments on its network. It has also announced an expanded partnership with OpenAI to accelerate these capabilities globally.

The commercial logic is straightforward: every AI agent that books, buys, or pays generates a transaction. Those transactions flow through Mastercard’s network. More AI adoption means more volume, more fees, without a single new human cardholder needed.

Disclaimer:

All information here is for educational purposes only. This is not financial advice. Please do your own research and speak with a licensed advisor before making any investment decisions. Past performance is not indicative of future returns. How we invest may not suit your investment goals and risk management profile.